Three approaches to e-invoicing: which one suits you?

Three diferent approaches are currently being pursued in the area of e-invoicing in order to meet industry- and country-specific requests, regulations, and deadlines. The following section describes the approaches as well as their pros and cons.

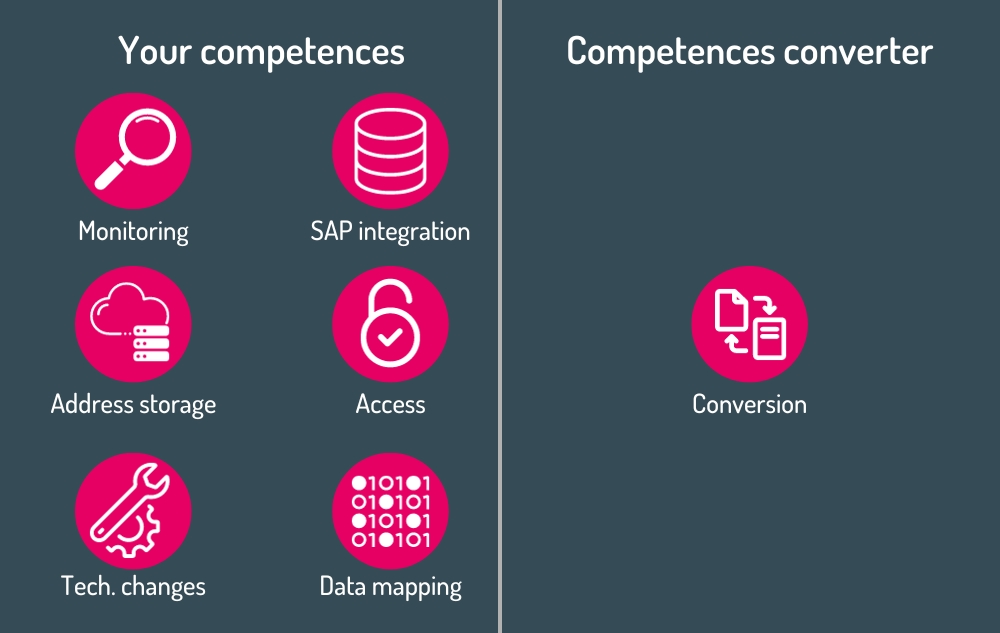

Approach via third-party converters

If companies use a third-party converter for their e-invoicing processes, only the data conversion is outsourced. All other tasks remain the responsibility of the company. This includes data mapping, storage of address information, setup of access points, implementation of technical changes, functional monitoring, and integration with SAP.

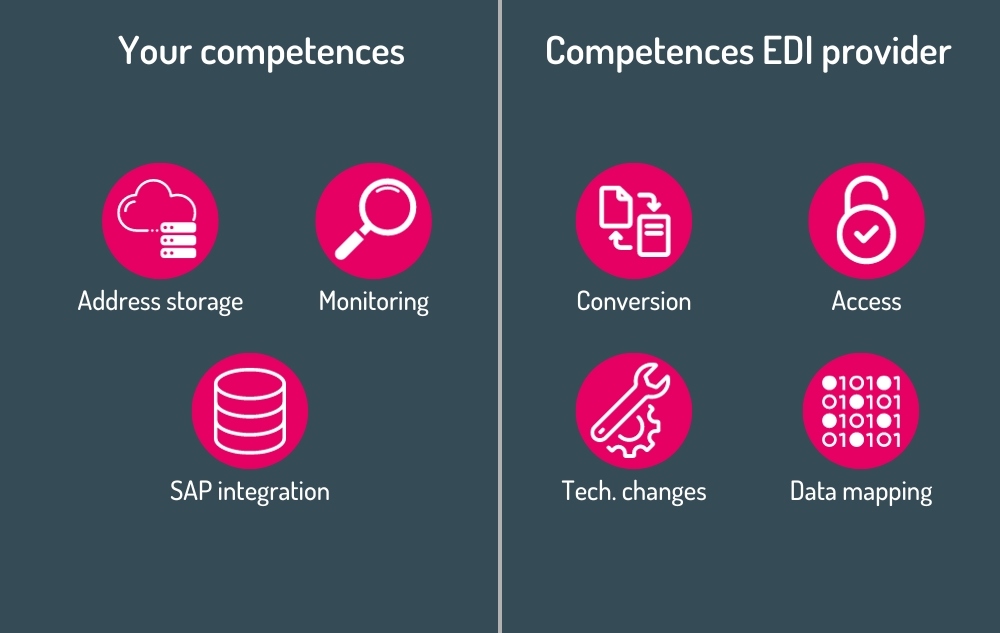

Approach via EDI provider

If companies rely on an external EDI provider, this provider is responsible for their data mapping, the implementation if technical changes, the setup af access points and the conversion of the e-invoicing data. Network connectivity, SAP integration, and functional monitoring and address storage remain the responsibility of the company.

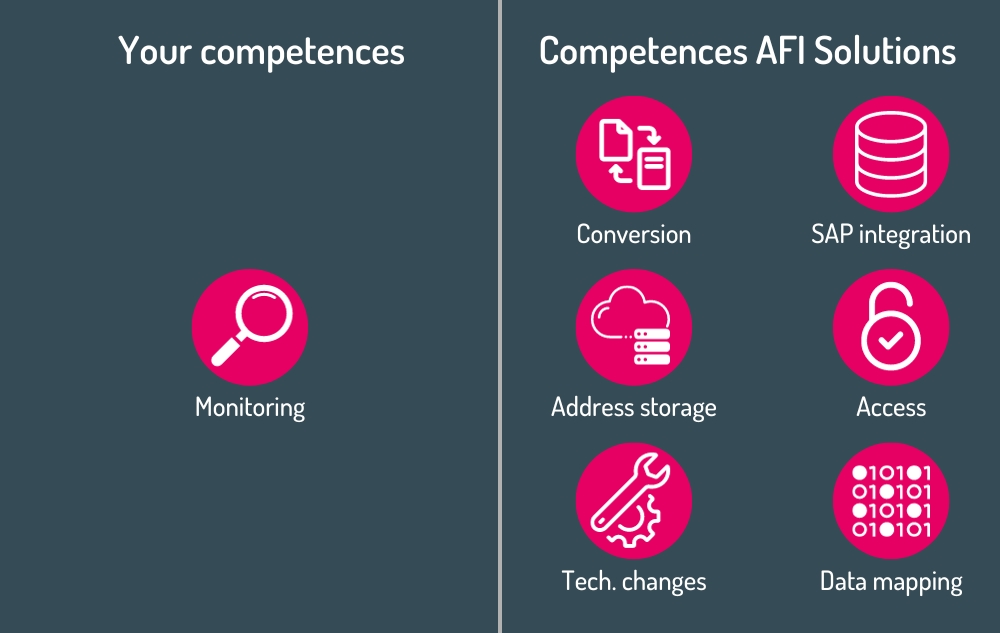

Approach via AFI Solutions

We have the required expertise and skills for data mapping, technical adjustments, access point configuration, data conversion, and address management in SAP integration. With AFI Solutions, the company is only responsible for the technical supervision. We also provide helpful features to relieve the burden further, e.g. the AFI Monitor.

Different e-invocing mandates for reporting in comparison

CTC vs. PTC: When it comes to e-invoicing and its regulations, companies also have to consider reporting obligations. There are two different models. But how are they different?

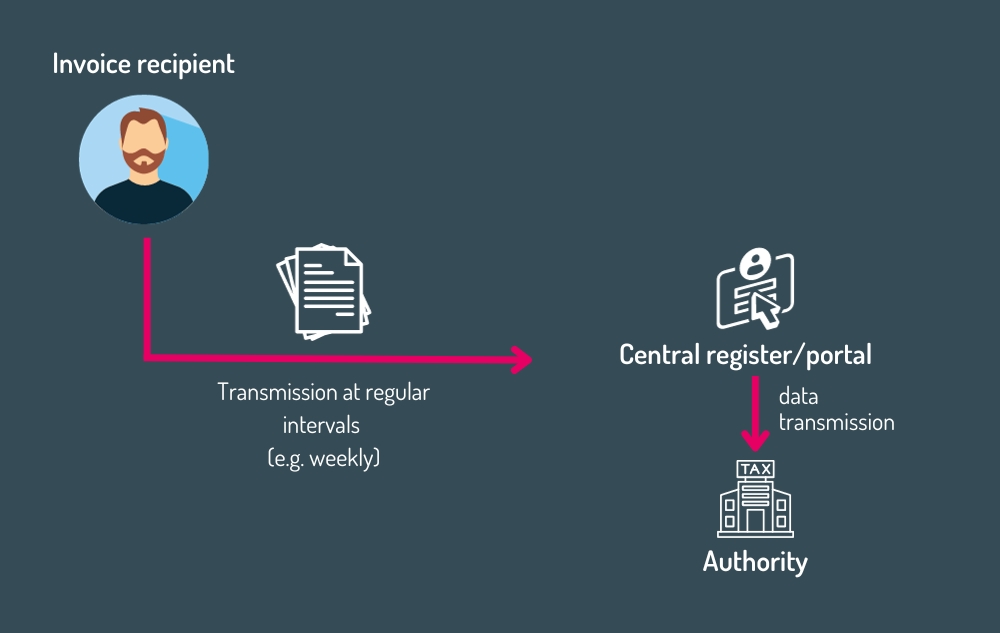

Periodic Transaction Control [PTC]

In contrast, there are countries that rely on the PTC approach. In this case, the relevant data is forwarded to the tax authorities at regular intervals (weekly, monthly, quarterly). Unlike continuous transmission, the e-invoicing data in the PTC process is collected first and then entered into the central reporting register.

V-model, Y-model, and reporting model: differences at a glance

The abovementioned models are approaches in electronic accounting. They serve to standardize the electronic invoicing process between companies and advance digitization. But what are the differences between the transmission models?

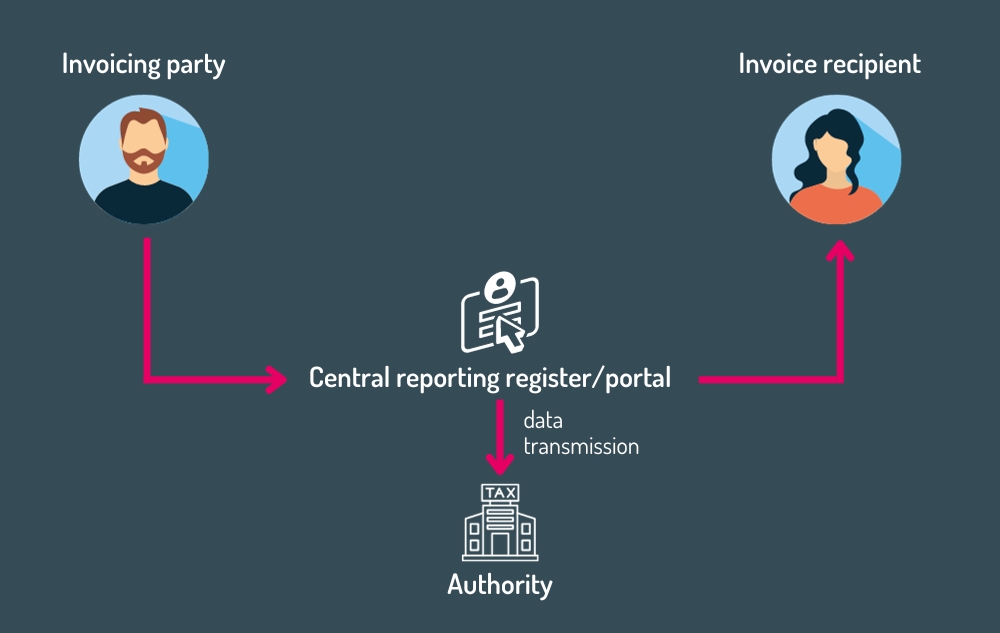

E-invoice route via the V-Model [CTC approach]

With the V-model, electronic invoices are forwarded by the invoicing party to the relevant authority by means of a central reporting register/portal. Subsequently, the invoice recipient receives the data of the basic business transaction either automatically forwarded or it is made available for independet download. Depending on the regulations of the countries, it is possible to use a private or state-certified interface for data transmission.

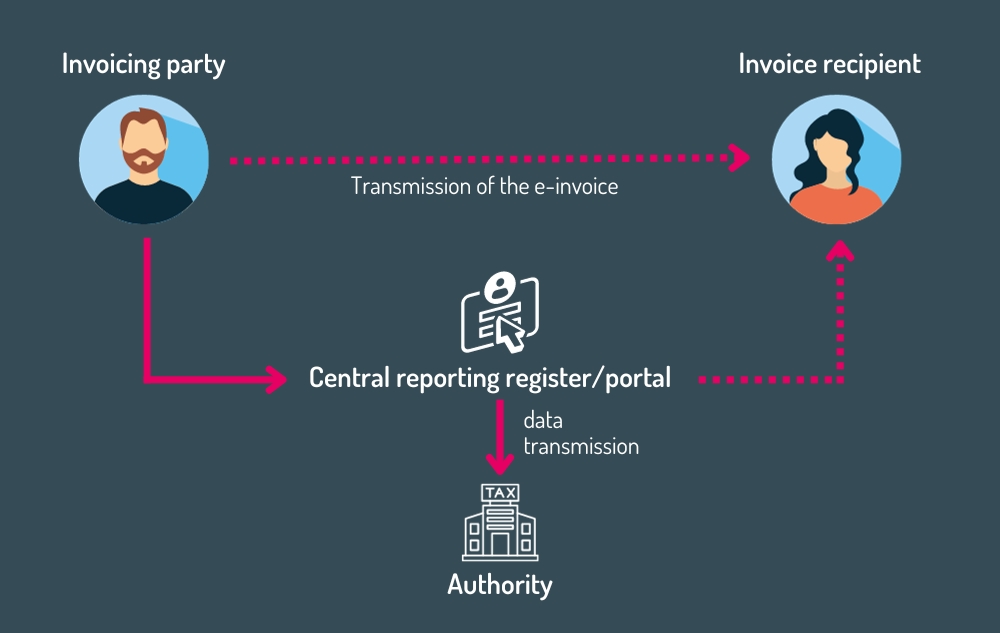

E-invoice route via the Y-model [CTC approach]

Invoicing parties have the option to transmitting the e-invoice directly to the recipient via a private or certified provider (e.g., PEPPOL) or using the central register/portal of the authorities. If invoicing parties opt for the former, they are required to additionally forward the e-invoice to the state financial administration or its official reporting portal in a further step.

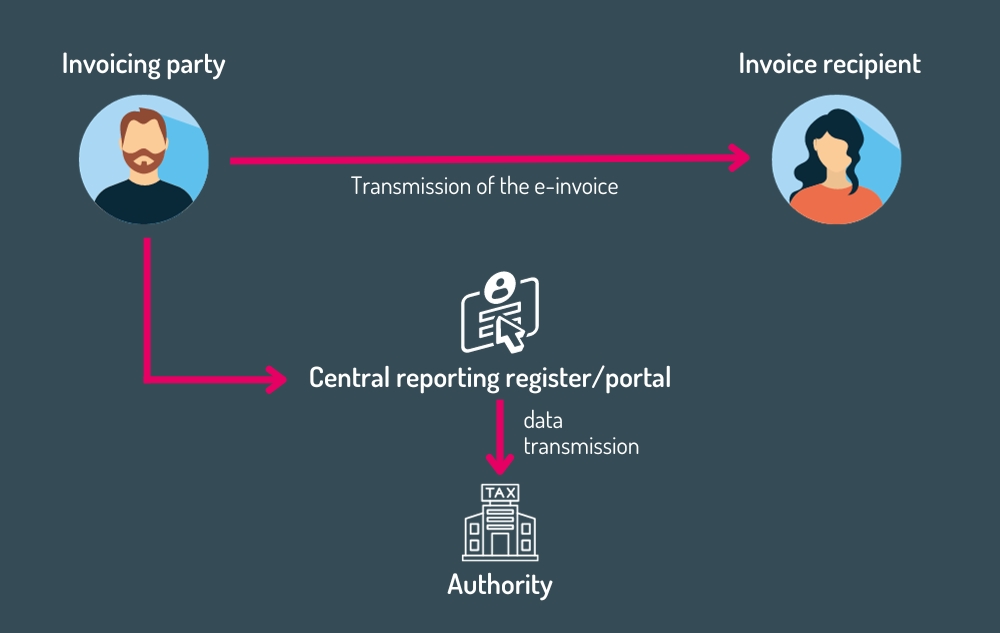

E-invoice route via the reporting model [CTC/PTC]

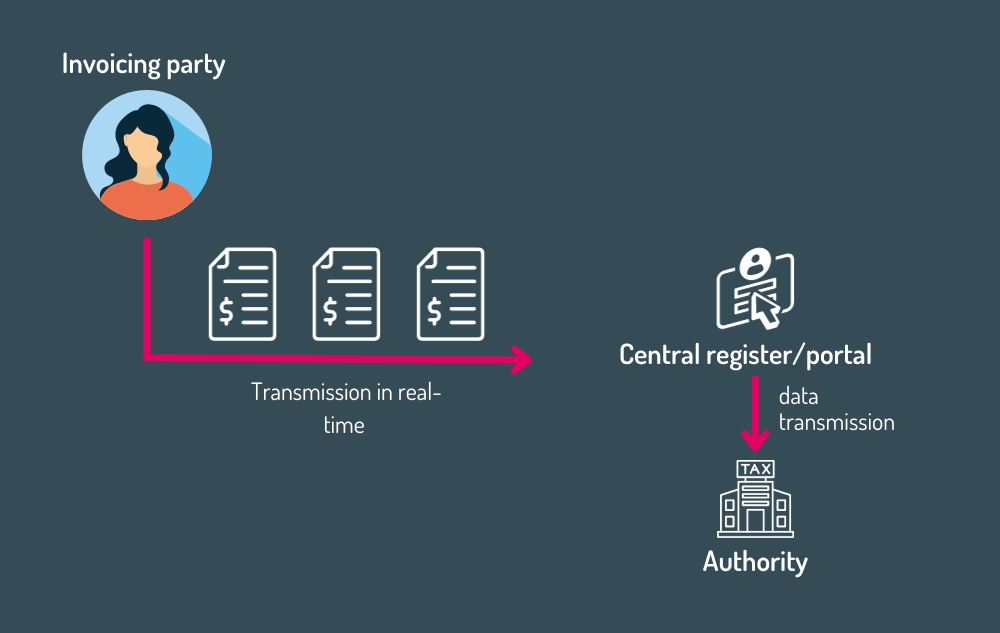

The reporting model is used in the context of cross-border invoicing. In contrast to the other two models, this model involves direct and exclusive transmission of the e-invoice from the invoicing party to the invoice recipient. The relevant transaction data is forwardes by the invoicing party in the respective e-invoice format to the central reporting register/portal and from there to the tax authority.

What about e-invoice formats?

E-invoice formats are divided into hybrid formats such as XML/PDF and structured formats such as XML.

- Hybrid formats XML/PDF

- ZUGFeRD/Factur-X

- In PDF integrierte XML

- Structured formats XML

- Primarily used

- Usually CII or UBL (technical distinction)

- PEPPOL-specific format (XML): used by serveral countries (usually Europe, exception: Japan)

Country specifics and deadlines

The topic of e-invoicing mandates is getting closer

Belgium

E-invoicing mandate as of 2026*

- E-invoicing mandate for B2B invoices according to the Y-Model

- E-invoice format: probably according to the PEPPOL 4-Corner-Model

France

Introduction date for e-invoicing as of september 2026*

- E-invoicing mandate for B2B invoices according to the V-Model

- E-invoice format: UBL, CII, Factur-X

Germany

E-invoicing mandate for receipt as of 2025*

- E-invoicing mandate for receipt as of January 2025

- E-invoice format: unknown

- Industry-specific EDIFACT formats (e.g. from Telekom, Vodafone, VW) valid until probably 2027

Italy

E-invoicing mandate since 2022

- E-invocing mandate for B2B and B2C invoices according to the V-Model

- E-invoice formate: FatturaPA

Poland

E-invoicing mandate as of the middle of 2026*

- E-invoicing mandate for B2B invoices according to V-Model

- E-invoice format: XML (KSeF)

Romania

E-invoicing mandate since 2022

- E-invoicing mandate according to V-model applies industry-specific: currently only for industries susceptible to corruption (e.g. alcohol, construction etc.)

- Extension of the mandate for further industries in 2024*

- E-invoce format: XML in the national standard RO_CIUS (UBL 2.1)

Serbia

E-invoicing mandate since 2023

- E-invoicing mandate for B2B invoices according to the V-Model

- E-invoice format: XML compliant with UBL 2.1

Slovakia

E-invoicing mandate as of 2025*

- E-invoicing mandate for B2B invoices according to V-Model

- E-invoice format: XML compliant with UBL 2.1

Why e-invoicing is becoming increasingly important

The clamor for e-invoicing mandates in the B2B sector is getting louder and louder. In many countries, new or more extensive obligations are already planned, and a lot is changing in the area of (international) transactions. But when does the e-invoicing mandate apply in which country? Which e-invocing transmission models are there and how do they differ from each other?

In a world where new regulations, technical changes and deadlines are constantly popping up, it can be difficult to track of everything. But don't worry, we've summarized the most important information for you below. Relevant topics include:

- Reporting

- Models

- Formats

- Country-specific information

- Approaches